After Lehman's Collapse: A Decade of Delay

Now that the 2018 midterms are over, folks can address the elephant in the room. If one tuned into Fox Business midday on January 7, one heard legendary corporate raider Carl Icahn dilate on the dimensions of the pachyderm, which he pegged at $250 trillion. That’s the size of worldwide debt. But can that be right -- it’s more than eleven times the official U.S. federal government’s debt? And in case you didn’t notice, it is a quarter of one quadrillion bucks. Pretty soon we’ll be talking real money.

Icahn’s $250T quotation for worldwide debt came out last year. On September 13, Bloomberg ran “$250 Trillion in Debt: the World’s Post-Lehman Legacy” by Brian Chappatta, who draws off data from the Institute of International Finance’s July 9 “Global Debt Monitor,” (to read IIF reports, one must sign up). Chappatta wonders how the world’s central bankers can “even pretend to know how to reverse what they’ve done over the past decade”:

[Central banks] kept interest rates at or below zero for an extended period […] and used bond-buying programs to further suppress sovereign yields, punishing savers and promoting consumption and risk-taking. Global debt has ballooned over the past two decades: from $84 trillion at the turn of the century, to $173 trillion at the time of the 2008 financial crisis, to $250 trillion a decade after Lehman Brothers Holdings Inc.’s collapse.

Chappatta breaks global debt down into four categories: financial corporations, nonfinancial corporations, households, and governments. In every category, global nominal debt rose from 2008 to 2018, with the debt of governments hitting $67T. In the important debt-as-a-percentage-of-gross-domestic-product measurement, three of the categories rose while only financial corporations fell, “leaving their debt-to-GDP ratio as low as it has been in recent memory.” Global banks seem to be “healthier and more resilient to another shock.” After reporting on worldwide debt, Chappatta then looks at U.S. debt.

What’s interesting about debt in America is that as a percentage of GDP, households and financial corporations have sharply reduced their debt. It is only government in America that has seen a sharp debt-to-GDP uptick, and it was quoted at more than 100 percent of GDP. That’s rather higher than for all government debt worldwide.

Besides the massive racking up of debt over the last decade there’s something else that should concern us: the massive creation of new money. One of the ways money is created is when central banks engage in the “bond-buying programs” that Chappatta refers to. We call such programs “quantitative easing.” When the Federal Reserve buys assets, like treasuries and mortgage-backed securities, it needs money. So the Fed just creates the money ex nihilo.

Besides the massive racking up of debt over the last decade there’s something else that should concern us: the massive creation of new money. One of the ways money is created is when central banks engage in the “bond-buying programs” that Chappatta refers to. We call such programs “quantitative easing.” When the Federal Reserve buys assets, like treasuries and mortgage-backed securities, it needs money. So the Fed just creates the money ex nihilo.

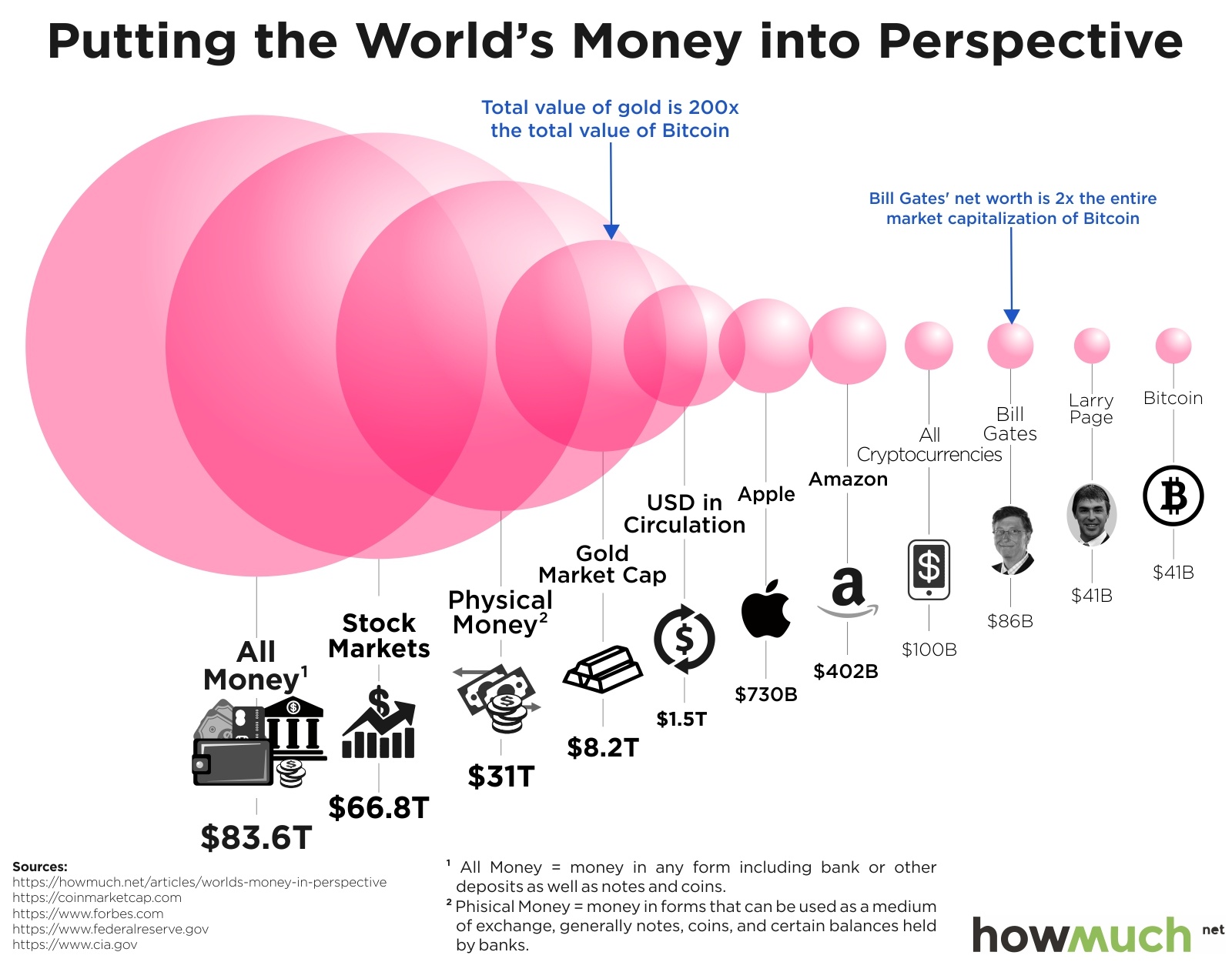

Since the U.S. isn’t the only nation that has been busy buying bonds and creating money, one might wonder just how much money there is in the world. In June of 2017, HowMuch put out “Putting the World’s Money into Perspective,” which is a nice little graphic that puts the category “All Money” at $83.6T.

{kind=link}

In November of 2017, MarketWatch ran “Here’s all the money in the world, in one chart” by Sue Chang, who in her short intro to the chart has some interesting things to say about global money, including cryptocurrencies. She writes of “narrow money” and “broad money” and pegs the latter at $90.4T, (or what Sen. Everett Dirksen would call “real money”.) If you want to examine Chang’s chart more closely, I’ve “excised” it here for your convenience; don’t miss the notes on the right margin. (Because its depth is 13,895 pixels, you might want to just save the chart to your computer rather than print it off.)

{kind=link}

So, in addition to an historic run-up in debt, there’s been a monster amount of new money created. Chappatta calls it the “grandest central-bank experiment in history.” His use of “experiment” is apropos, as one wonders whether the world’s central bankers and their economists really know what they’ve been doing.

One ray of hope might just be President Trump’s choice of Jerome Powell as Chairman of the Federal Reserve, (Trump has such good instincts about people). One can get a sense of the man from his January talk with David Rubenstein at the Economic Club of Washington, D.C. (video and transcript). It’s refreshing that Mr. Powell disdains the “Fed speak” used by his predecessors.

Chappatta’s article is quite worth reading, and it’s not very long. The charts are user-friendly, although animated ones are a bit “creative.” The last section, “China Charges Forward,” is especially worthwhile.

This is the post-Lehman legacy. To pull the global economy back from the brink, governments borrowed heavily from the future. That either portends pain ahead, through austerity measures or tax increases, or it signals that central-bank meddling will become a permanent fixture of 21st century financial markets.

Given those alternatives, let’s try a little austerity. But austerity would entail spending cuts, and Congress has a poor history in that regard. In fact, since fiscal 2007, the year before the financial crisis, total federal spending has gone from $2.72T a year to more than $4T. While austere citizens deleverage and get their fiscal affairs in order, Congress shamefully borrows and spends like never before.

Congress’ solutions are to bail out, prop up, and do whatever it takes to avoid reforming what it has created. So they farm out their responsibilities to the Federal Reserve. Indeed, in the July 17, 2012 meeting of the Senate Banking Committee (go to the 53:50 point of this C-SPAN video), Chuck Schumer told Federal Reserve Chairman Ben Bernanke the following:

So given the political realities, Mr. Chairman, particularly in this election year, I'm afraid the Fed is the only game in town. And I would urge you to take whatever actions you think would be most helpful in supporting a stronger economic recovery… So get to work, Mr. Chairman. (Chuckles.)

So the Fed is “the only game in town” because there are only monetary solutions for the economy, right? There aren’t any fiscal solutions, as they would involve Congress, and Congress is busy running for re-election, right? Sounds like you’re abdicating your responsibilities, Chuck.

The last decade has been an exercise in delay. Congress has avoided doing the difficult and unpopular things that would help avoid future financial collapses. If Congress were serious about balancing the budget, then social programs would be on the chopping block, because that’s where the real money goes.

Jon N. Hall of ULTRACON OPINION is a programmer from Kansas City.

FOLLOW US ON